The world of consumer finance is on the move, shifting away from its paper roots and embracing the digital age. This journey towards digitization is reshaping how we think about everything from banking to borrowing. However, amidst this wave of change, one ancient relic of the past stubbornly remains in use: the coupon book. Many lenders still rely on these physical booklets to facilitate loan repayments, a method that increasingly creates friction, especially among younger generations who may find this process outdated and unfamiliar.

For digital natives, or the younger generation that has grown up in a world saturated with digital technology, the concept of a coupon book feels alien. Accustomed to the convenience and immediacy of digital transactions, these individuals often perceive traditional, paper-based methods as inefficient and unnecessarily complicated. This can lead to frustration and a diminished customer experience, potentially impacting the lender-borrower relationship negatively.

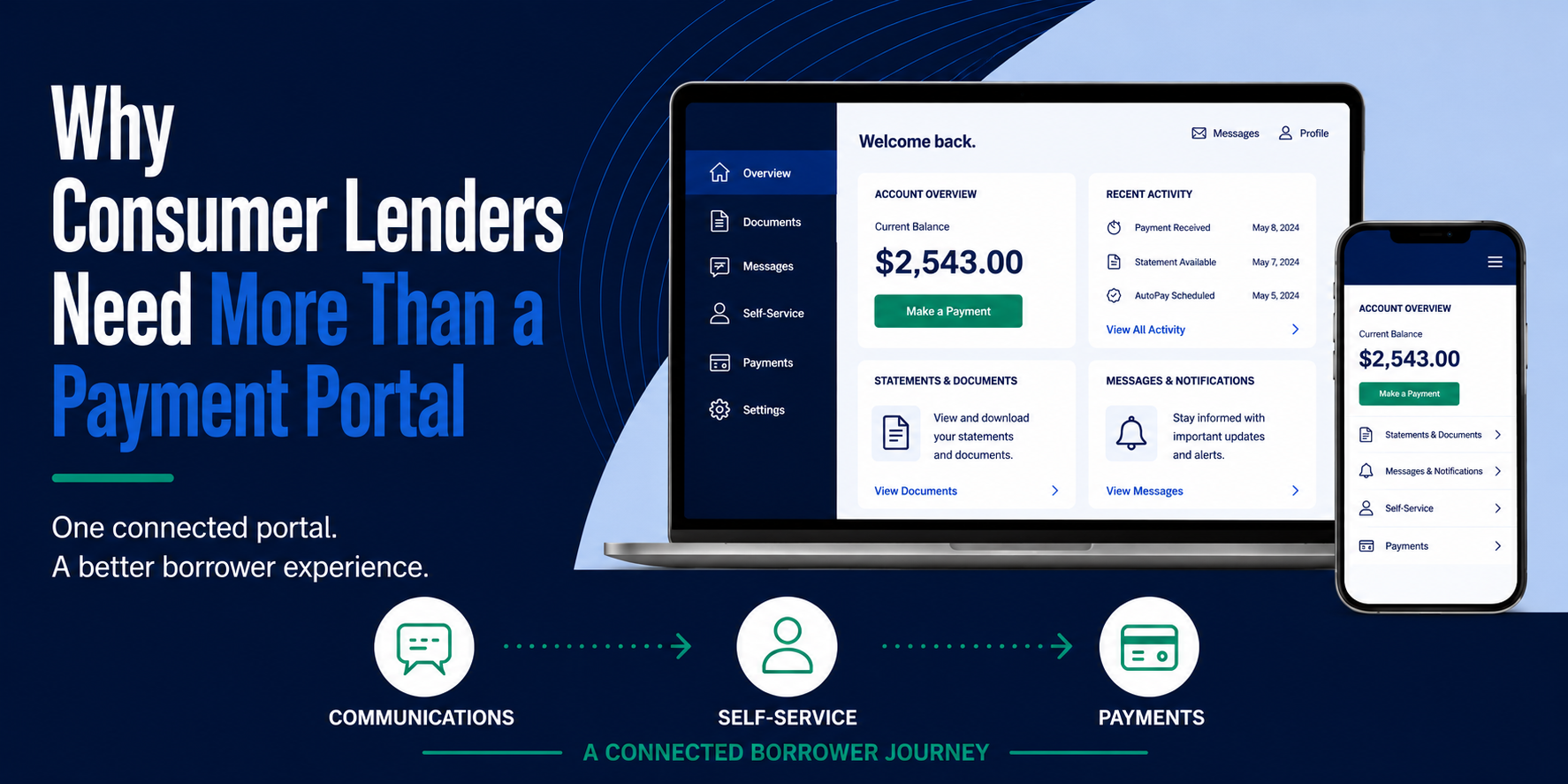

The good news is that there is a better way to manage the bill/pay process, one that does not necessitate sending monthly statements or clinging to outdated coupon books. The solution lies in embracing digital payment platforms and communication channels that align with modern consumer behaviors and expectations.

.png?width=700&height=100&name=Banner%20-Technology%20Boosts%20Compliance%20in%20Consumer%20Finance%20Communications%20(5).png)

Benefits of Digital Payments Transformation:

Increased Efficiency and Convenience: Digital channels offer borrowers the ease of making payments anywhere, anytime, without the need for physical paperwork.

Enhanced Customer Experience: A smooth, user-friendly digital payment process improves overall satisfaction, fostering loyalty among customers.

Reduced Environmental Impact: Moving away from paper-based processes not only aligns with sustainability goals but also resonates with the growing eco-consciousness among consumers.

Improved Payment Tracking and Management: Digital platforms provide both lenders and borrowers with real-time access to payment histories, outstanding balances, and other critical financial information.

Keeping the Personal Touch in a Digital World

Transitioning to digital payment methods does not mean losing the personal touch that many consumers value in their interactions with financial institutions. On the contrary, digital platforms can be designed to deliver personalized communication and support, tailored to the unique needs and preferences of each borrower. By leveraging data analytics, lenders can gain insights into customer behavior, enabling them to customize their outreach and offerings effectively.

Embracing the Future of Digital Payment Solutions

For lenders willing to leave the era of coupon books behind, the path forward involves integrating digital payment solutions that are secure, reliable, and user-friendly. It's about creating a seamless, frictionless payment experience that meets the demands of today's digital-first consumers while laying the foundation for future innovations.

As the consumer finance industry continues to evolve, the adoption of digital payment methods will no longer be a competitive advantage but a necessity. The time to act is now—lenders must embrace this digital shift or risk being left behind in a world that is increasingly moving online.

In conclusion, the transition from coupon books to digital payment channels represents more than just a technological upgrade; it signifies a commitment to meeting the changing needs of consumers in a digital age. For lenders, this shift offers an opportunity to enhance operational efficiency, improve customer satisfaction, and secure a competitive edge in the dynamic landscape of consumer finance.

Break free from the constraints of outdated billing and payment systems and streamline your bill/pay process ! See how...

.png)